Quick Summary

In a family business divorce North Carolina case, you may see courts evaluate ownership interests, marital contributions, and business structure before dividing the assets. Judges examine whether the business is marital or separate property and how control is exercised. Understanding these factors helps you see how closely held companies may be evaluated during equitable distribution in North Carolina divorce proceedings.

In a family business divorce North Carolina case, courts determine whether the business is marital property, separate property, or partly both. This classification affects whether the business may be divided between spouses.

You may see judges review when the business started, how ownership shares are structured, and whether marital funds or labor contributed to its growth.

North Carolina follows equitable distribution rules, meaning assets are divided fairly rather than automatically split equally. Guidance from North Carolina Divorce Attorneys at Martine Law often helps individuals understand how courts interpret these ownership questions.

How Equitable Distribution Applies To Closely Held Businesses

Equitable distribution determines how marital assets are divided in a divorce. When a closely held business is involved, courts analyze how the company fits into the marital estate.

In closely held business equitable distribution NC cases, judges often examine several factors:

- Whether the business was created before or during the marriage

- Contributions made by either spouse to business growth

- Use of marital funds to support the company

- Financial value of ownership shares

North Carolina law provides the framework courts use when evaluating marital property. The state’s property division statutes explain how equitable distribution applies to assets such as businesses.

How Courts Distinguish Marital And Separate Business Interests

In a family business divorce North Carolina case, courts first determine whether the business qualifies as marital property or separate property. This classification is important because only marital assets are typically subject to equitable distribution during divorce proceedings.

Several factors may influence whether a business interest is considered separate, marital, or partially both.

Business Classification | Typical Situation | Possible Effect in Divorce |

Separate Property | Business started before the marriage and maintained independently | Usually remains with the original owner spouse |

Marital Property | Business created during the marriage using marital resources | May be included in equitable distribution |

Hybrid Interest | Business existed before marriage but increased in value during marriage | Increase in value may be considered marital property |

Courts may also review whether a spouse contributed labor, management, or financial support to the company during the marriage. These contributions can influence how the business interest is classified and whether any portion of the business value becomes part of the marital estate.

In some situations, spouses may also need to demonstrate ownership history through tracing separate property, which helps establish whether certain assets originated from inheritance or pre-marital ownership.

Evaluating Control Rights Within A Family Business

Ownership and control are not always identical in family-owned companies. Courts may distinguish between economic ownership and management authority when evaluating how a business operates during divorce proceedings.

Even when both spouses hold ownership interests, one spouse may exercise greater decision-making authority within the company. Judges may review several aspects of the business structure to understand how control functions in practice.

These considerations may also influence how business ownership is addressed during property division in North Carolina divorce cases.

Voting Rights Linked To Ownership Interests

Voting rights attached to ownership shares may influence which spouse has authority over key business decisions. Courts may review shareholder agreements, membership interests, or corporate governance documents to determine how voting power is structured within the business.

Operating Agreements Defining Business Management Authority

Operating agreements or partnership agreements often outline how management authority is distributed among owners. These documents may clarify which individuals are responsible for daily operations, financial decisions, and long-term strategic planning.

Each Spouse’s Role In Business Management

Courts may also consider whether both spouses actively participated in managing the business during the marriage. Evidence of involvement in operations, financial oversight, or leadership roles may help judges evaluate how control and responsibilities were shared within the company.

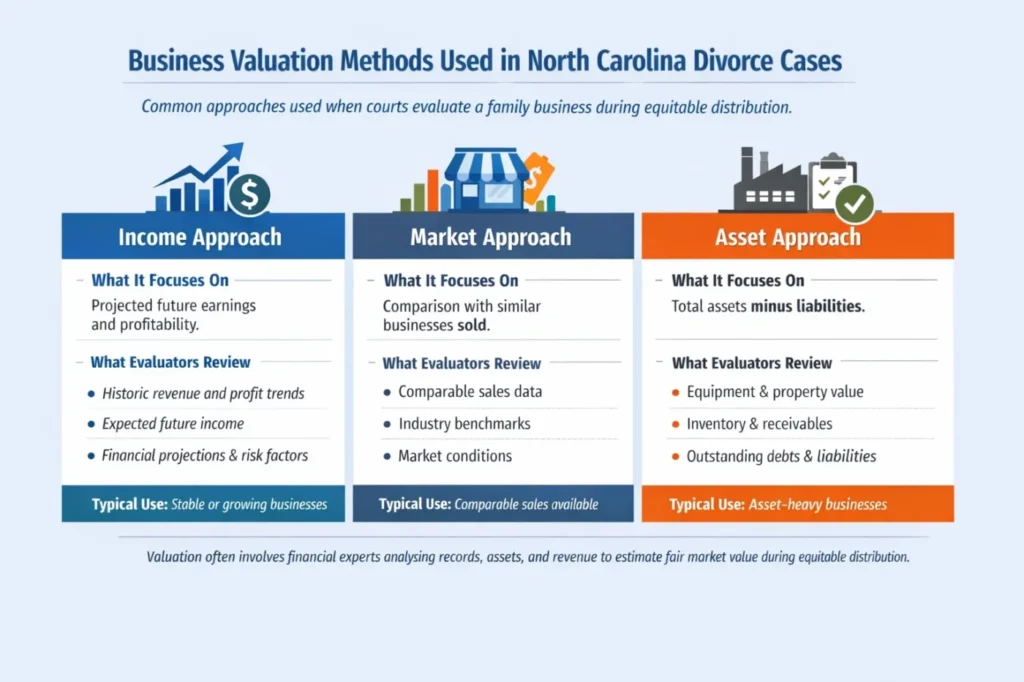

Business Valuation Methods Courts May Consider In Divorce

Before a business can be divided, its financial value typically must be determined. Courts rely on professional valuation methods to estimate the company’s worth.

Common valuation approaches include:

- Income approach: evaluates projected earnings

- Market approach: compares similar businesses sold in the market

- Asset approach: reviews company assets minus liabilities

Source: North Carolina Judicial Branch – Equitable Distribution

Financial experts often assist courts in determining business value. The court procedures provided by the North Carolina Judicial Branch explain how property issues are addressed during divorce cases.

How Courts Handle Family Business Division Outcomes

After determining value and ownership, courts decide how the business should be handled in the divorce settlement. In a family business divorce North Carolina case, the outcome often depends on the company’s structure, the financial interests of both spouses, and whether continued involvement in the business is practical.

In many cases, courts aim to balance fairness between spouses while also considering the stability of the business itself. When a closely held company is involved, judges may evaluate whether dividing ownership could disrupt operations or affect the company’s long-term viability.

You may see several possible outcomes:

- One spouse buys out the other’s interest, allowing the business to remain under a single owner

- Ownership remains with one spouse while other marital assets are used to offset the business value

- Spouses retain partial ownership under structured agreements that define responsibilities and profit distribution

- The business is sold, and the proceeds are divided between the spouses

These outcomes depend on fairness considerations, the financial circumstances of each spouse, and whether continued joint ownership would be practical after the divorce. Courts may also consider how different division approaches could affect the company’s operations and long-term financial stability.

Factors Judges Review When Dividing Business Interests

Judges consider multiple legal and financial factors before deciding how business ownership should be distributed in divorce cases.

In closely held business equitable distribution NC matters, courts often evaluate how each spouse contributed to the company and whether dividing ownership could affect the business’s stability.

Judges may review several elements, including:

- Each spouse’s financial contributions to the business

• Time spent managing or working in the company

• The potential impact of divorce on daily operations

• Tax consequences that may arise from transferring ownership

These factors help courts assess fairness while also considering whether the business can continue operating effectively after the divorce.

By reviewing both financial contributions and operational involvement, judges attempt to balance equitable distribution principles with the practical need to maintain the viability of the business.

Know More: Equitable Distribution Factors: Judicial Discretion in Unequal Division of Marital Assets

Financial Records And Documents Often Reviewed by Court

Business division in divorce cases often requires detailed financial information. Courts typically review various records to determine the company’s value, ownership structure, and whether marital funds or efforts contributed to the business during the marriage.

These documents help judges understand how the company was formed, how it operates, and how its financial value developed over time.

Common records examined include:

- Corporate formation documents

- Partnership or shareholder agreements

- Business tax returns

- Financial statements and profit reports

- Ownership certificates or membership interests

Accurate financial documentation allows courts to trace the business’s development and evaluate its financial performance. In some situations, reviewing these records may also reveal hidden assets that could affect how marital property is evaluated during equitable distribution.

Identifying undisclosed income, ownership interests, or financial transfers can be important when courts assess whether the full value of a business has been properly disclosed during divorce proceedings.

Understanding Business Division In North Carolina Divorce

Dividing a family-owned business during divorce often requires courts to review ownership history, financial contributions, and the structure of the company. In a family business divorce North Carolina case, judges may determine whether the business is marital or separate property and how its value should be addressed under equitable distribution rules. Courts may also examine financial records, control rights, and each spouse’s role in managing or supporting the company during the marriage. These factors help courts evaluate how the business developed and whether it should be divided, transferred, or offset with other marital assets.

Practical Guidance On Business Division In Divorce

If you would like more information about how business ownership may be evaluated in a family business divorce North Carolina matter, you may contact the North Carolina Divorce Attorneys at Martine Law at +1 (704) 255-6992 or visit the Contact Us page

FAQs

Can one spouse keep the family business after divorce?

Yes, one spouse may retain ownership of the business if the court determines that the arrangement is appropriate. In many cases, the spouse who continues operating the company may keep it while the other spouse receives assets of similar value. In closely held business equitable distribution NC cases, courts often consider fairness and whether transferring ownership could affect the company’s financial stability.

How do courts determine the value of a family-owned business?

Courts often rely on financial experts to evaluate the company’s value during divorce proceedings. These professionals may review financial statements, tax filings, ownership documents, and operational records to estimate the business’s worth. Valuation methods may vary depending on the company’s structure, income history, and assets. This process helps judges understand how the business fits within the marital estate

What happens if asset tracing cannot clearly identify business ownership?

When the ownership records and financial histories are incomplete, judges may rely on available evidence to determine how the business interest relates to the marriage. Issues involving commingled funds can make it more difficult for courts to determine whether part of a business interest should be treated as marital property.

Can a family business remain jointly owned after divorce?

Yes, in some situations spouses may continue owning a business together after divorce. Courts may allow joint ownership when both parties agree on management responsibilities and financial arrangements. However, ongoing cooperation is often necessary to avoid disputes. In a family business divorce North Carolina case, courts may also evaluate whether continued shared ownership could affect the company’s operations or long-term stability.