Quick Summary

In a separate property divorce NC case, inheritances and family gifts may remain individually owned if clear proof shows they were intended for one spouse and kept separate from marital assets. Courts examine documents, financial records, and how the property was handled during the marriage. Understanding how these claims are evaluated helps you recognize what evidence may support inheritance or family gift classification.

In North Carolina divorce cases, inheritances and family gifts may qualify as separate property if they were intended for one spouse and kept separate from marital finances.

Courts review documentation, financial history, and the way assets were managed during the marriage to determine whether a claim fits the rules of separate property divorce NC classifications.

Disputes sometimes arise when inherited funds are deposited into joint accounts or used to purchase shared property. Judges then examine whether the original separate status was preserved.

In family law matters involving asset classification, North Carolina Divorce Attorneys at Martine Law explain how courts review evidence related to inheritances, family gifts, and financial records during property division.

Legal Definition Of Separate Property In North Carolina

Separate property generally refers to assets owned by one spouse individually and not subject to division during divorce. In North Carolina, inheritances and personal gifts may qualify as separate property when they are clearly intended for only one spouse and kept distinct from marital assets.

Courts review how the asset was acquired and whether it remained separate throughout the marriage. If the asset was mixed with marital funds or used jointly, its classification may become disputed.

The state’s separate property rules explain how courts evaluate property ownership and determine whether a gift or inheritance remains separate rather than becoming marital property subject to equitable distribution during divorce proceedings.

How Courts Distinguish Inheritances From Marital Property

Courts distinguish inheritances from marital assets by reviewing how the property was received and handled during the marriage. The central question is whether the inheritance remained separate or became combined with marital funds.

Judges evaluate ownership records, financial transactions, and the way the asset was used over time to determine whether it still qualifies under separate property divorce NC rules.

Common Factors Courts Review

Factor Courts Examine | Indicator of Separate Property | Indicator of Marital Property |

Ownership at transfer | Inheritance directed to one spouse | Asset transferred to both spouses |

Account handling | Funds kept in an individual account | Funds deposited into a joint account |

Use of funds | Not used for marital expenses | Used for shared purchases or debts |

Property title | Asset titled in one spouse’s name | Property titled jointly |

Value changes | Growth from market factors | Increase caused by marital contributions |

If inherited funds were deposited into shared accounts or used for joint purchases, courts may require financial tracing to determine whether the asset can still be recognized as separate property. Issues involving mixed financial sources are often discussed in cases involving commingled funds, where asset tracing becomes necessary to determine ownership.

Documentation Used To Prove Separate Property Claims

Courts rely heavily on documentation to verify inheritance or family gift claims. Written evidence helps establish both ownership and the intent behind the transfer.

In separate property divorce NC cases, judges review financial and legal records to confirm that an asset was intended for one spouse and remained separate during the marriage. Clear documentation helps courts evaluate both the origin of the property and how it was managed over time.

Common documents examined include:

- Wills or estate distribution documents

- Trust records showing the beneficiary

- Bank transfer records or deposit confirmations

- Letters or written statements describing a gift

- Financial account statements tracing the asset

These records help demonstrate that the property qualifies as separate and was not intended to become marital property during the marriage.

Know More – Tracing Separate Property: Proving Inheritance and Pre-Marital Assets in NC Divorces

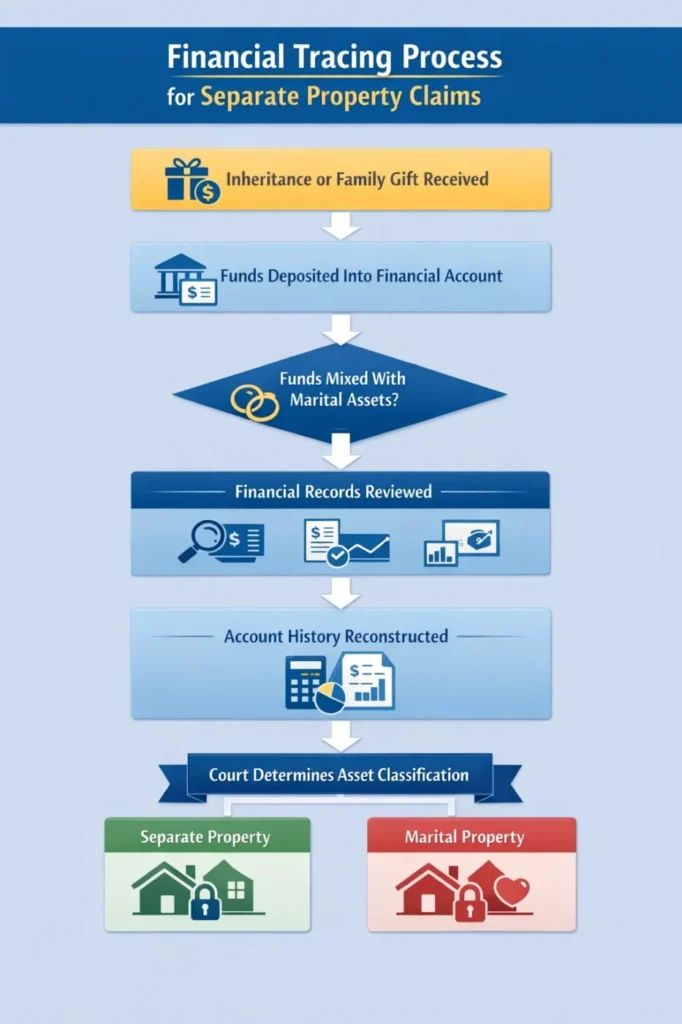

Why Is Financial Tracing Often Becomes Necessary

Financial tracing is necessary when separate and marital property are mixed. Courts use tracing to follow the movement of funds and determine whether an asset originally came from inheritance, a gift, or another separate source.

When financial accounts contain both marital and separate funds, judges review account histories and transaction records to determine whether the asset still qualifies under separate property divorce NC rules.

Source: North Carolina Judicial Branch – Equitable Distribution Guide

Tracing may become necessary in several common situations:

- Inheritance money was deposited into joint accounts

- Separate funds were used to purchase shared property

- Investments were made using mixed financial sources

In inheritance divorce NC cases, courts sometimes rely on accountants or financial experts to reconstruct account histories. By reviewing financial statements, transfers, and investment records, experts help determine whether the original inheritance or family gift maintained its separate status throughout the marriage.

How Courts Evaluate Intent Behind Family Gifts

Family gifts are treated differently from inheritances but often follow similar legal principles when courts evaluate property classification. The key question usually concerns the donor’s intent at the time the gift was made.

Judges examine available evidence to determine whether the gift was meant for one spouse individually or for the marriage as a whole. Clear documentation and consistent handling of the property often play an important role in how courts interpret the gift during equitable distribution proceedings.

Evidence Courts Use To Identify Donor Intent

Judges commonly review several indicators to determine how a family gift should be classified during a divorce case. These details help clarify whether the property was meant for one spouse individually or for both spouses together.

Common indicators courts review include:

- Whether the gift was directed to one spouse or both spouses

- Written messages or documentation accompanying the gift

- Testimony from the person who provided the property

These factors help judges understand the circumstances surrounding the gift and the intention behind it when evaluating property division during divorce proceedings.

How Property Use Can Affect Gift Classification

Courts also evaluate how the gifted property was used after it was received. How the property is handled during the marriage may determine whether it remains separate or becomes marital property.

For example, a financial gift from a parent intended specifically for one spouse may qualify as separate property when evidence supports that intention.

However, if the funds were deposited into a joint account or used for shared household expenses, courts may review whether the property was effectively treated as marital during the marriage and therefore subject to property division.

Situations When Separate Property Status Can Change

Separate property may lose its individual classification in certain circumstances during a divorce. This often occurs when the asset becomes integrated into marital finances or treated as jointly owned during the marriage.

During financial investigations into hidden assets, courts may review records and transactions to determine how property was handled and whether separate funds were commingled with marital assets.

Common situations where this may happen include:

- Depositing inherited funds into joint bank accounts

- Using separate money to renovate a jointly owned home

- Placing inherited assets in both spouses’ names

When these situations occur, courts analyze whether the original property was commingled with marital assets. If the funds or property were mixed in ways that make ownership difficult to trace, the court may examine financial documentation to determine how the asset should be classified during divorce proceedings.

Evaluating Caregiving Roles Within Household Structure

Courts also review how caregiving responsibilities are shared within the household. When a third party regularly participates in supervision, routines, or emotional support, judges may evaluate how that involvement contributes to the child’s daily environment.

In some cases, these caregiving roles may also affect how courts review parenting schedules and visitation arrangements, which are explained further in parenting time schedules. This review helps courts understand how responsibilities are distributed within the family structure.

Credibility Considerations In Custody Disputes

During custody disputes, courts may also consider how each party presents information about the child’s care and household routines. Statements about caregiving roles, supervision, and involvement may be reviewed alongside other evidence presented to the court.

These considerations help judges evaluate the overall parenting environment while reviewing custody arrangements.

Relationship Between Separate Property And Asset Division

Separate property claims are closely connected to the broader process of dividing marital assets during divorce. Before courts determine how assets will be distributed, they must first identify which property is considered marital and which remains separate.

This classification step helps ensure that only marital assets are included in the division process. If an inheritance or family gift qualifies as separate property, it is generally excluded from asset division.

However, the spouse claiming the property as separate must provide sufficient evidence to support that position. Courts may review financial records, documentation, and testimony to confirm whether the asset maintained its separate status throughout the marriage.

Understanding Separate Property Claims In Divorce Cases

In many divorce cases, inheritances and family gifts raise questions about whether an asset should remain individually owned or become part of marital property.

Courts evaluate documentation, financial history, and the intent behind the transfer to determine whether the property qualifies under separate property divorce NC rules.

Clear records and consistent handling of inherited assets often play a central role in these decisions.

Speak With North Carolina Divorce Attorneys

If you would like more information about how separate property divorce NC claims involving inheritances or family gifts are evaluated, North Carolina Divorce Attorneys at Martine Law can provide guidance on how courts review these financial records and legal standards. You may call +1 (704) 255-6992 or visit the Contact Us page to discuss your situation.

FAQs

Can inherited money become marital property in North Carolina?

Yes. Inherited money can become marital property if it is mixed with marital funds or treated as shared property during the marriage. In separate property divorce NC cases, courts review how the inheritance was handled. Depositing funds into joint accounts, using them for marital purchases, or placing them in both spouses’ names may affect whether the asset remains separate.

Do courts require written proof for inheritance claims?

Yes. Courts often rely on written proof to confirm that property was inherited and intended for one spouse. Documents such as wills, estate records, and bank transfers help verify the origin of the asset. In inheritance divorce NC disputes, clear documentation may help demonstrate that the inheritance qualifies as separate property rather than marital property.

What happens if assets are discovered late in a divorce?

Courts may review whether an asset should have been disclosed earlier if new property is discovered during the divorce process. Judges often allow updated documentation or amended filings before finalizing property division. The timing of the disclosure and available evidence may influence how the asset is classified. In some situations, late asset claims may require additional court review.

Are gifts from family always considered separate property?

No. Family gifts are not always treated as separate property. Courts review whether the gift was clearly intended for one spouse alone or for both spouses. If the gift was addressed to both spouses or later treated as shared property during the marriage, judges may classify the asset differently when evaluating property ownership in divorce proceedings.